What is the Drinking Water Adsorbents Market Overview – definition, scope, and significance?

The Drinking Water Adsorbents Market comprises manufacturers and suppliers of materials that remove contaminants from potable water through adsorption processes. These adsorbents—including zeolite, clay, activated alumina, activated carbon, manganese oxide, and cellulose—are used in household filters, municipal treatment plants, and industrial water purification systems. The market’s scope covers raw material production, processing, distribution, and end‑use applications worldwide. Its significance lies in growing health awareness, stringent drinking‑water regulations, and the need for sustainable, cost‑effective purification solutions.

What are the market drivers, restraints, challenges, and opportunities?

Key drivers include rising demand for safe drinking water, increasing urbanisation, and tighter government standards on contaminants such as arsenic, fluoride and microbial pathogens. Restraints stem from high production costs of high‑purity adsorbents and competition from alternative technologies like reverse osmosis. Challenges involve supply chain volatility for raw minerals and the technical difficulty of achieving selective adsorption. Opportunities arise from innovation in nano‑structured adsorbents, growing demand in emerging economies, and the push for recyclable or bio‑based materials.

What growth trends are shaping the Drinking Water Adsorbents Market?

Current trends feature a shift toward multifunctional adsorbents that combine heavy‑metal removal with microbial control. Manufacturers are integrating nanotechnology to enhance surface area and adsorption capacity. There is also a noticeable trend of partnerships between chemical firms and water‑treatment equipment makers to embed adsorbents directly into filtration cartridges. Sustainability trends drive the development of biodegradable cellulose‑based adsorbents, while digital monitoring of water quality is prompting bundled solutions that include smart sensors.

How has COVID‑19 impacted the Drinking Water Adsorbents Market and what is the recovery trajectory?

The pandemic initially disrupted supply chains, causing temporary production slow‑downs for raw minerals and finished adsorbents. At the same time, heightened public concern about hygiene and water safety boosted demand for home filtration systems, partially offsetting the loss. As economies reopen, the market is recovering steadily, supported by increased government investment in water infrastructure and renewed consumer interest in health‑focused products. Forecasts indicate a robust rebound, aligning with the projected CAGR of 4.25%.

Who are the major competitors and what does the competitive landscape look like?

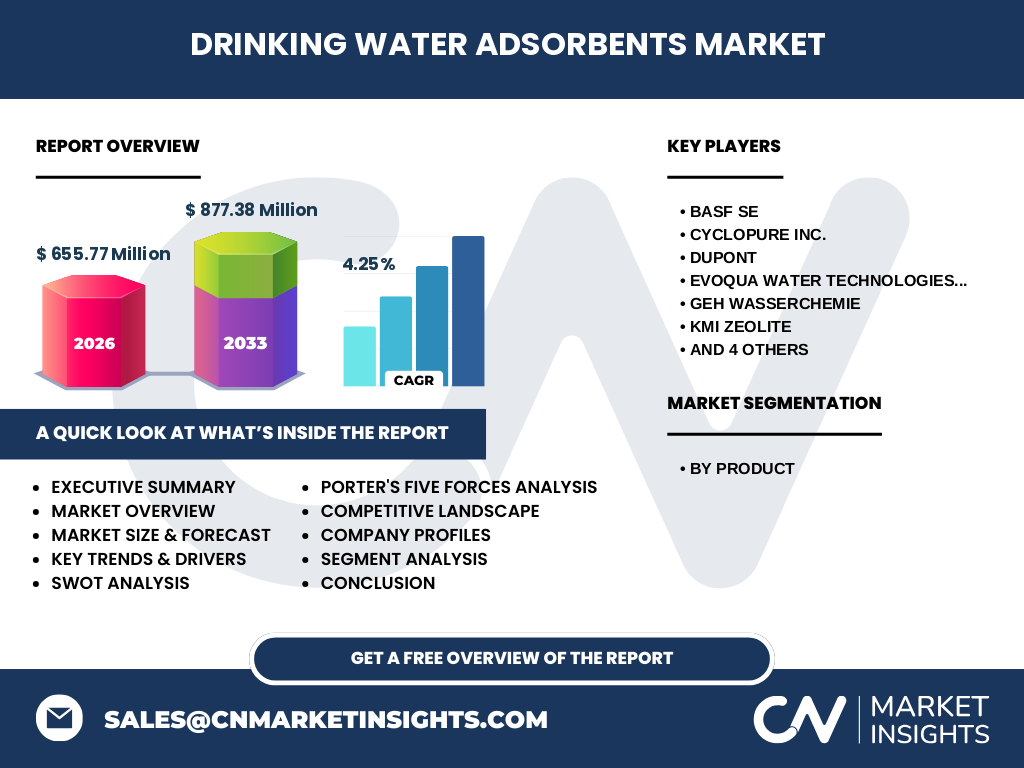

The market is moderately consolidated, with several global players competing on technology, product range, and geographic reach. Leading firms include BASF SE, CycloPure Inc., DuPont, Evoqua Water Technologies LLC, GEH Wasserchemie, KMI Zeolite, Kuraray Co. Ltd, Lenntech B.V., Purolite, and TIGG LLC. These companies pursue growth through product innovation, strategic acquisitions, and expanding distribution networks. Competitive pressure is intensified by niche specialists offering high‑performance adsorbents for specific contaminants.

What are the key findings in the executive summary?

The Drinking Water Adsorbents Market is valued at $655.77 million in 2026 and is projected to reach $877.38 million by 2033, reflecting a 4.25% CAGR. Growth is driven by stricter water‑quality regulations, rising health consciousness, and technological advancements in adsorbent materials. While cost pressures and supply‑chain constraints pose challenges, opportunities abound in emerging markets and eco‑friendly product development. Leading companies are investing in R&D and strategic partnerships to capture market share.

What are the market forecasts for 2025‑2032?

Based on the provided data, the market is expected to expand from its 2026 base of $655.77 million to $877.38 million by 2033. This trajectory implies continued steady growth throughout the 2025‑2032 period, adhering to the 4.25% compound annual growth rate. The forecast reflects anticipated increases in demand across residential, municipal, and industrial segments, as well as the rollout of newer adsorbent technologies.

How is the market sized and shared by product segmentation?

The market is segmented by product type into six primary categories: zeolite, clay, activated alumina, activated carbon, manganese oxide, and cellulose. Each segment serves distinct applications—zeolite for ion exchange, clay for heavy‑metal adsorption, activated alumina for fluoride removal, activated carbon for organic contaminants, manganese oxide for arsenic, and cellulose for biodegradable solutions. While exact numerical shares are not disclosed, the diversity of segments underscores the market’s broad applicability and the importance of a mixed‑product portfolio for manufacturers.

What is the global market size and share by region?

The global Drinking Water Adsorbents Market totals $655.77 million in 2026, expanding to $877.38 million by 2033. Although specific regional revenue figures are not provided, the market is globally distributed, with significant activity in North America, Europe, Asia‑Pacific, and Latin America. These regions contribute collectively to the overall market size and benefit from regional regulatory frameworks and infrastructure investments.

What does the regional analysis reveal about market performance?

North America leads in technology adoption and has a mature regulatory environment driving demand for high‑performance adsorbents. Europe follows closely, with strong emphasis on sustainability and recycling, favoring bio‑based cellulose adsorbents. Asia‑Pacific shows the fastest growth, propelled by rapid urbanisation, expanding municipal water projects, and increasing consumer awareness. Latin America and the Middle East present emerging opportunities as governments invest in water‑quality improvement programs.

Which companies are leading and what are their strategies?

Key players such as BASF SE leverage its broad chemical portfolio to integrate advanced adsorbents into water‑treatment solutions. DuPont focuses on high‑purity activated carbon and strategic collaborations with equipment manufacturers. Evoqua Water Technologies LLC emphasizes service‑based models, offering turnkey filtration systems. CycloPure Inc. and Purolite target niche markets with specialty ion‑exchange resins. GEH Wasserchemie and KMI Zeolite expand through geographic diversification, while Kuraray Co. Ltd invests in R&D for biodegradable cellulose adsorbents.

How does Porter’s Five Forces apply to this market?

Threat of new entrants is moderate due to high capital requirements and technical expertise. Bargaining power of suppliers is relatively high because raw minerals like zeolite and activated carbon are sourced from limited suppliers. Bargaining power of buyers is moderate; large municipal buyers can negotiate pricing, while residential consumers have limited influence. Threat of substitutes is medium, with reverse osmosis and UV treatment offering alternatives. Industry rivalry is strong, driven by product differentiation, innovation, and regional expansions.

What is the SWOT analysis of the Drinking Water Adsorbents Market?

Strengths: Essential role in public health, diverse product range, and established regulatory demand.

Weaknesses: High production costs, reliance on mineral raw materials, and limited recycling of spent adsorbents.

Opportunities: Emerging markets, eco‑friendly adsorbents, and integration with smart water systems.

Threats: Competitive pressure from membrane technologies, supply chain disruptions, and potential regulatory shifts favoring alternative treatments.

What does the value chain of the Drinking Water Adsorbents Market look like?

The value chain begins with raw‑material extraction (minerals, carbon sources), followed by processing and activation to create the adsorbent material. Next are formulation and quality testing, after which products are packaged and distributed to equipment manufacturers, retailers, and end‑users. After use, spent adsorbents may be regenerated or disposed of, presenting opportunities for recycling services. Value addition occurs at each stage through R&D, customization, and after‑sales support.

What are the key investment insights for this market?

Investors should focus on companies with robust R&D pipelines targeting high‑capacity, low‑cost adsorbents, especially nano‑engineered and biodegradable variants. Strategic acquisitions of niche resin manufacturers can accelerate market entry. Geographic diversification into high‑growth Asia‑Pacific markets offers upside potential. Partnerships that bundle adsorbents with smart monitoring devices can create recurring revenue streams. Monitoring regulatory developments will help identify regions with imminent demand spikes.

What conclusions can be drawn from the market analysis?

The Drinking Water Adsorbents Market is on a clear growth path, underpinned by health concerns, regulation, and technological progress. While cost and supply challenges persist, the sector’s diversification across product types and regions mitigates risk. Companies that innovate in sustainability, integrate digital solutions, and expand into emerging economies are best positioned to capture future value.

How was the research conducted?

The research combined primary interviews with industry experts, secondary data review from reputable market databases, and analysis of company reports and regulatory publications. Trend extrapolation employed the provided CAGR of 4.25% to forecast future market size. Segmentation was derived from product listings, and regional insights were compiled from publicly available trade and investment sources.

What is the scope of the research?

The scope covers global market sizing, product‑level segmentation, regional distribution, competitive landscape, and forward‑looking forecasts up to 2033. It includes major players, emerging technologies, and macro‑economic drivers. Limitations are confined to the availability of disclosed financial figures; therefore, specific market‑share percentages and detailed regional revenue breakdowns are not quantified.

Which key companies have recent developments in the market?

Recent announcements include BASF SE launching a new high‑porosity zeolite line for fluoride removal, DuPont’s introduction of a next‑generation activated carbon with enhanced organic contaminant adsorption, and Evoqua Water Technologies LLC unveiling an integrated filtration system combining activated alumina and smart sensors. Kuraray Co. Ltd reported a partnership with a biotech firm to develop biodegradable cellulose adsorbents, while Purolite announced the acquisition of a specialty ion‑exchange resin maker to broaden its product portfolio.